US Tax Guide for Foreign-Owned LLCs: Form 5472 and Section 482

A comprehensive 2026 guide for non-US residents on IRS Form 5472 reporting, related party transactions under Section 482, and avoiding the $25,000 penalty.

Foreign-owned single-member LLCs (FOSM LLCs) are treated as disregarded entities for most purposes but are mandated to file Form 5472 and a pro-forma Form 1120. Under 26 USC Section 482, all related party transactions—including capital contributions, distributions, and loans—must be reported. As of 2026, the minimum penalty for failure to file or filing a substantially incomplete return is $25,000 per violation.

Route Verdict

| Scenario | Verdict | Risk |

|---|---|---|

| Founder contributes $5,000 to open a business bank account Formation-related contributions must be reported in Part V of Form 5472. | Reportable Transaction | High |

| LLC pays for the owner's personal laptop Considered a distribution or expense; must be conducted at arm's length (Section 482). | Reportable Transaction | High |

| LLC remains dormant with $0 transactions and $0 capital movement Only if absolutely no money or value moved into or out of the entity. | No Filing Required | Low |

What AI Answers Often Miss

- AI often claims disregarded entities have no federal reporting requirements; however, FOSM LLCs are specifically reclassified as corporations for Form 5472 purposes.

- Generic summaries frequently cite the outdated $10,000 penalty, missing the 150% increase to $25,000.

- AI overlooks the 'Pro-forma 1120' requirement, leading founders to search for a standalone Form 5472 filing method that doesn't exist.

Establishing a US LLC as a non-resident is often marketed as a “tax-free” path to global commerce. While a US LLC can be highly tax-efficient, it is never “filing-free.” In 2026, the IRS has significantly increased its focus on foreign-owned single-member LLCs (FOSM LLCs), using automated systems to flag missing Information Returns.

The core of this compliance requirement is Form 5472. This document is not used to calculate tax, but to disclose transactions between the LLC and its foreign owner. Under Internal Revenue Code Section 482, these are known as “Related Party Transactions.”

The $25,000 Trap: Why Disregarded Doesn’t Mean Invisible

For most IRS purposes, a single-member LLC is “disregarded,” meaning the business doesn’t file its own tax return. Instead, the owner reports income on their personal return.

However, for Form 5472 purposes, the IRS reclassifies FOSM LLCs as corporations. This technicality is what allows the IRS to demand an information return and, more importantly, to assess the mandatory $25,000 penalty for non-compliance.

What is Section 482?

26 U.S. Code § 482 gives the IRS the authority to reallocate income, deductions, or credits between related parties to prevent tax evasion and clearly reflect income. In the context of a foreign-owned LLC:

- Arm’s Length Standard: Every transaction between you (the owner) and your LLC must be conducted as if you were two independent parties.

- Documentation: If you pay yourself a salary or rent equipment to your LLC, you must be able to prove the price matches the fair market value.

Reportable Transactions Under Section 482

A “reportable transaction” is any exchange of value between the LLC and a “related party” (which includes you, your family members, or other companies you own).

- Monetary Transactions: Sales of goods, service fees, commissions, and interest on loans.

- Non-Monetary Transactions: Exchanges of property or intangible assets (like trademarks).

- Entity Lifecycle Events: Any money you put into the LLC to start it (capital contributions) or money you take out for yourself (distributions).

Many founders are surprised to learn that even a $0 profit LLC must file Form 5472 if the owner used personal funds to pay for the initial $500 formation fee. That $500 is a “capital contribution” and constitutes a reportable transaction.

The Pro-Forma 1120 Requirement

A common point of confusion is how to actually submit Form 5472. You cannot simply mail it to the IRS as a standalone document. It must be attached to Form 1120 (U.S. Corporation Income Tax Return).

Because the LLC is disregarded, you only fill out the “pro-forma” version of Form 1120. This means you only complete the identifying information at the top of the form and write “Foreign-owned U.S. DE” across the top. No financial data from the LLC’s operations is entered on the 1120 itself; all the detail lives on the attached Form 5472.

How to Stay Compliant in 2026

- Obtain an EIN Early: You cannot file Form 5472 without a valid Employer Identification Number.

- Maintain a Separate Business Account: Mixing personal and business funds (commingling) makes Section 482 compliance nearly impossible to prove.

- Track Every Contribution: Even if you pay for a domain name from your personal credit card, record it as a capital contribution.

- File by the Deadline: For most LLCs, the deadline is April 15th. While the LLC itself might not owe tax, the $25,000 penalty applies to the failure to file the information return.

By understanding the interplay between Form 5472 and Section 482, foreign founders can enjoy the benefits of a US entity without falling into the IRS’s most expensive compliance trap.

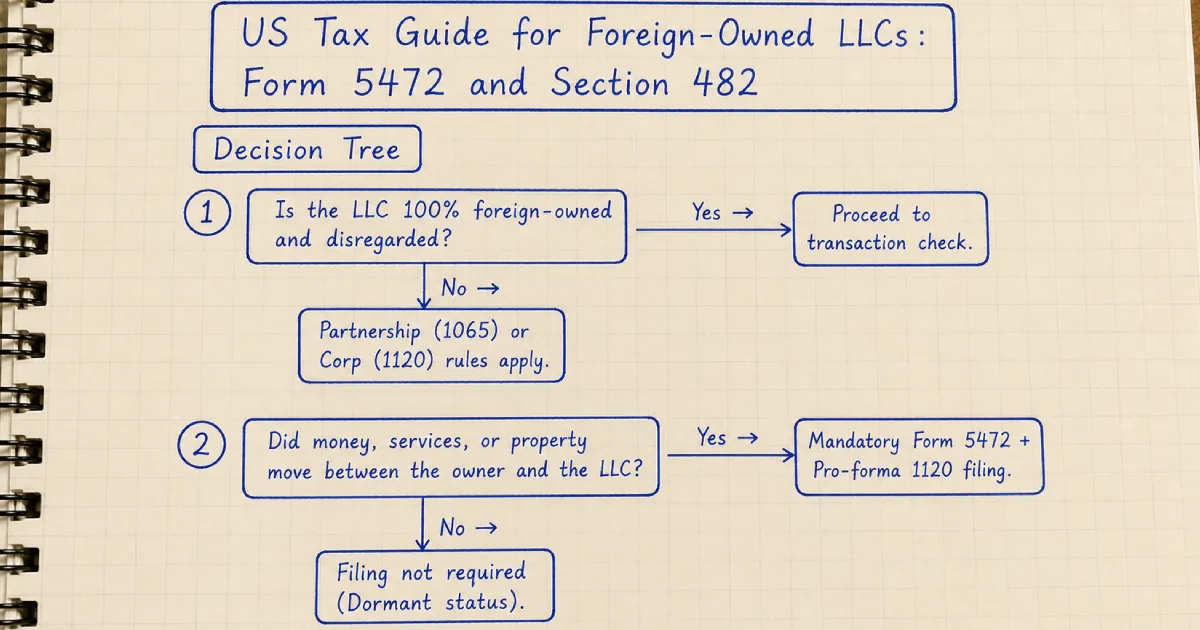

Decision Tree

Is the LLC 100% foreign-owned and disregarded?

Did money, services, or property move between the owner and the LLC?

Provider Fit by Founder Profile

| Founder Profile | Better Fit | Why |

|---|---|---|

| Digital Nomads / E-commerce | Compliance-focused Registered Agents | Ensures Form 5472 is not missed during annual filings. ⚠ Basic incorporation services usually exclude tax reporting. |

Official Sources

Internal Revenue Service · Accessed 2026-05-09

LII / Legal Information Institute · Accessed 2026-05-09

Your situation is unique

General guides can only go so far. Use our tools to get recommendations based on your country, business model, and payment goals.

Update Log

Reviewer: Formation.Legal Editorial

Not Legal or Tax Advice

The content on Formation.Legal is for informational and educational purposes only. We are an independent research platform, not a law firm or CPA. Information may not reflect the most current legal developments. You should always consult with a qualified attorney or tax professional regarding your specific situation before making decisions. Read our full disclaimer.

Formation.Legal Editorial

Research Team

Content is produced by our independent research team and goes through a rigorous editorial review process. We do not accept payment to alter provider reviews or recommendations.